Table Of Content

- Factors Affecting Your Down Payment

- Faster, easier mortgage lending

- Rocket Sister Companies

- Mortgage Pre-Approval

- Do I need to have the down payment in cash, or can I use other assets as collateral?

- Average down payment on a house for first-time homebuyers

- What mortgage programs allow for low down payments?

- How can you save for a down payment?

Every article is based on rigorous reporting by our team of expert writers and editors with extensive knowledge of products. High-yield savings accounts (HYSAs) can earn more than 5% interest while still allowing you to make withdrawals if something unexpected happens. Western Alliance Bank's HYSA currently earns an APR of 5.32%, one of the highest CNBC Select has reviewed. You only need a dollar to open an account, and there's no minimum balance requirement or monthly fees. You can also speed up the saving process by setting up automatic money transfers on certain days of the month (e.g. on payday twice per month).

Factors Affecting Your Down Payment

Participating national banks and credit unions may also offer first-time home buyer grants. Depending on the program, you can use the funds for various purposes, such as covering your down payment, closing costs or necessary improvements and repairs. The average down payment for a house differs widely by state due to different home prices. Additionally, the age of home buyers also plays a factor, as older buyers tend to have more money. The National Association of Realtors (NAR) states that the average down payment on a house for first-time home buyers is 6% versus 17% for repeat buyers in 2022.

Faster, easier mortgage lending

Five percent down exceeds the minimum requirements for conventional and government-backed mortgages. Lenders also check your credit score, income, and debt to make sure you qualify. A lender could require a higher down payment based on these factors. PMI rates on conventional loans vary depending on your down payment amount and your credit score. Typical PMI rates can range from less than 0.5% of the loan amount up to 1.86% annually. That annual fee is broken into monthly payments that are included in your mortgage payment.

Rocket Sister Companies

2 rules to consider when deciding how much mortgage you can afford, according to a financial planner - CNBC

2 rules to consider when deciding how much mortgage you can afford, according to a financial planner.

Posted: Thu, 25 Apr 2024 07:00:00 GMT [source]

However, eligible borrowers can put down as little as 3% but pay additional fees. The Federal Housing Administration offers FHA loans to first-time buyers, where homebuyers only have to contribute a down payment of 3.5% of the purchase price. FHA loans are enticing for buyers who need capital after closing a deal, but not all buyers qualify for these programs. If a single Californian is purchasing a home for themselves, they must make less than $95K. Two people buying a house together cannot earn over $150,000 combined before taxes if they plan to use FHA loans. A lower down payment typically also means you won’t qualify for the lowest possible mortgage rate.

Buyers can either pay a monthly premium for the insurance or a one-time upfront premium when a deal closes. Some lenders provide conventional loans and will not require PMI, but the interest rate may vary as a result. Figuring out your credit score helps determine what percentage of purchase price lenders may require for a down payment. The average down payment for a house in California typically ranges between 15% to 20% of the purchase price, but can vary depending on your mortgage lender and financial situation.

Do I need to have the down payment in cash, or can I use other assets as collateral?

We’ll also discuss the average amount buyers pay upfront so you can get an idea of what to expect on your journey toward homeownership. Many lenders recommend a DTI below 43%, but some programs allow a maximum of 50%. Additionally, having a good credit score of 670 or above helps you qualify for lower rates and fees, as lenders perceive less risk. Home buyers are posting smaller down payments in most housing markets since home prices peaked in the fourth quarter of 2022 and are decreasing through 2023 year-to-date. The median down payment on a home in the U.S. was $51,250 as of December 2023, according to real estate data provider ATTOM, an 8.6 percent increase year-over-year. The offers that appear on this site are from companies that compensate us.

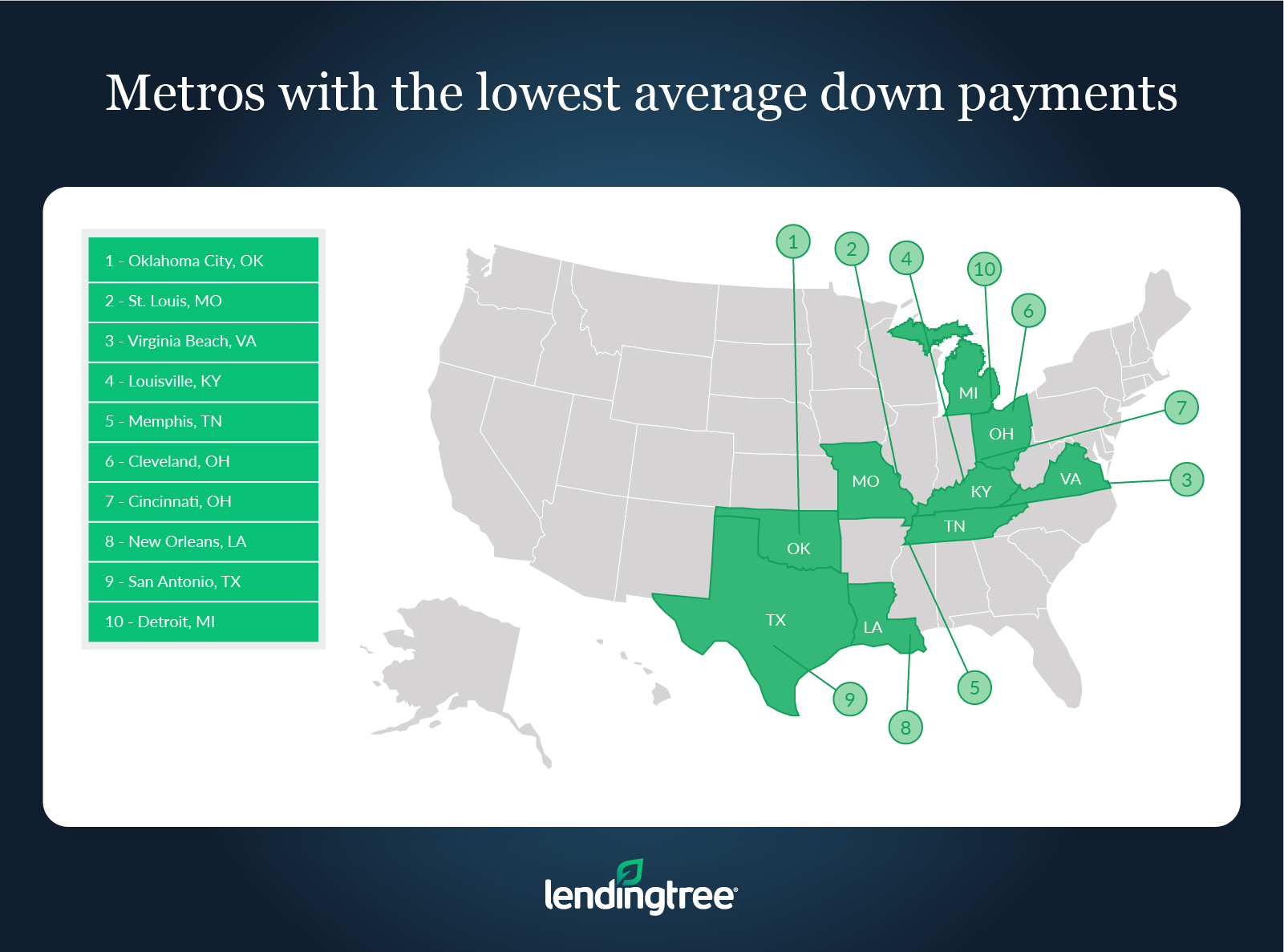

Average down payment on a house for first-time homebuyers

And, with some loan programs, it’s possible to make a down payment of three or even zero percent. In fact, the median down payment on a home is only 13% according to the National Association of Realtors (NAR). If these numbers seem steep, remember the amounts will be lower for a house below this price point. After all, plenty of people — especially first-time home buyers — are house-hunting below the $400,000 mark. Rates on new home loans now far surpass rates locked in by Americans with existing mortgages. Simultaneously to the swift pivot in mortgage rates, home values have been spiking.

The good news is that you can buy a house with less than 20% down though it is a good idea to put down as much as you can. Here are some of the considerations when thinking about how much of a down payment you may need for your dream house. Get expert tips, strategies, news and everything else you need to maximize your money, right to your inbox. A down payment is the portion of the home price the borrower pays upfront.

And if you’re just short on funds, there are down payment assistance programs that can help. That’s $850 for every $100,000 borrowed — or $2,550 for a loan balance of $300,000. This amount of money would be broken down into monthly payments of about $212.

While some buyers in California may pursue down payment assistance programs if they qualify, others turn to family for help with their down payment and closing costs. For example, if you purchase a $1,500,000 home in La Jolla, expect to make a down payment of at least $225,000 to $300,000 on average. While some buyers want to put more money down to reduce monthly payments, many first-time homebuyers in California ask how they can reduce their initial down payment. Mortgages issued by lenders require an investment of capital from buyers to secure financing, and the type of loan dictates the required down payment. Buyer’s brokers commonly field questions about how much should be saved up for a down payment when buying a home in California, and the answers differ for all buyers.

But not all buyers want to lower their down payment, as providing more equity upfront reduces interest rates and chips away at the principal. Regardless of the type of loan, buyers should shop around when looking for mortgages. VA loan programs from the Department of Veterans Affairs provide access to zero percent down at closing, so long as buyers stay within financial limits set on a county by county basis.

Even if your first-time homebuyer down payment can’t reach that 20 percent mark, buying might still make sense. Once you have enough equity (usually, 20 percent), you can ask your servicer to get rid of your mortgage insurance. As we noted above already, the minimum down payment requirements for a home can vary based on the type of home loan you've picked, your credit score, and other factors. The down payment requirements for a conventional loan on a primary residence vary depending on the lender, the borrower and the property type. For example, first-time homebuyers and buyers with low to moderate incomes could qualify for a fixed-rate conventional loan with a 3 percent down payment.

You'll need at least a 620 credit score to be considered, however, and have an annual income that doesn't exceed 80% of the median income in your area. • A larger down payment can result in lower monthly mortgage payments and potentially better loan terms. • The amount of the down payment can vary based on factors like loan type, credit score, and lender requirements. • The average down payment on a house in the US is around 6-20% of the purchase price. The organization estimates that closing costs can tack on another 2% to 5% of the sales price of a home, or $6,000 to $15,000 in closing costs for a home worth $300,000. Make sure you have this cash set aside, or else you'll have to pull it from the down payment amount you save up.

No comments:

Post a Comment